Gold vs High-Yield Savings Accounts: Why 4% APY Can't Compete with 70% Returns

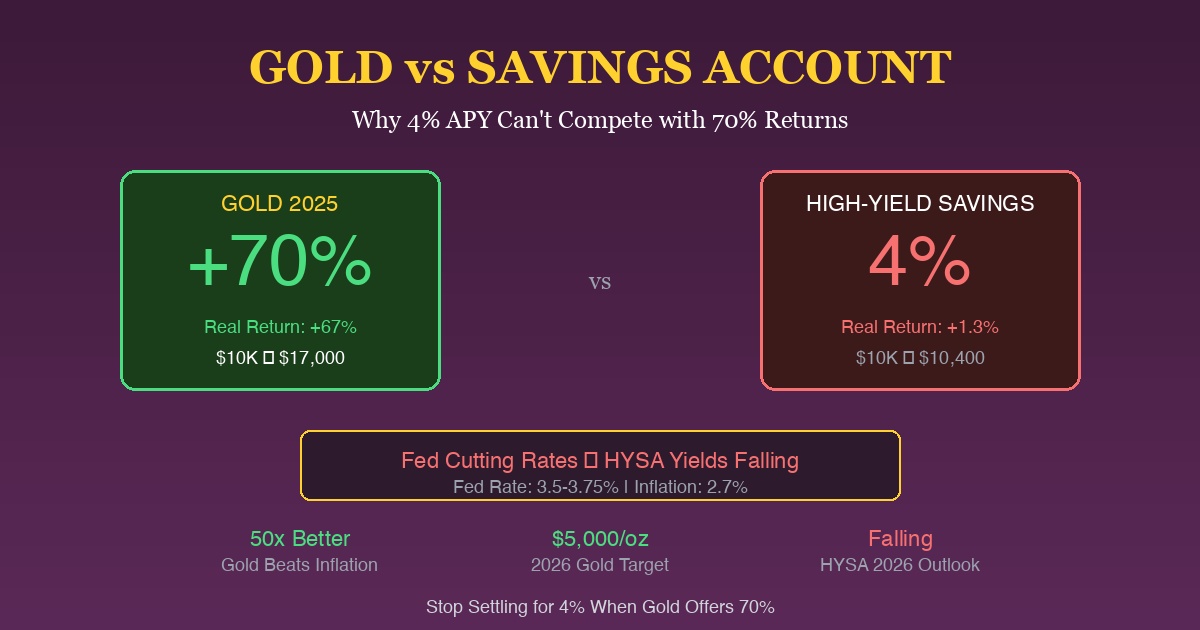

Your high-yield savings account is earning 4% APY. Gold returned 70% in 2025. While you watched your savings compound at a rate barely above inflation, gold investors saw their wealth nearly double. As the Federal Reserve continues cutting rates—now at 3.5%-3.75% after three consecutive cuts—savings account yields are falling. Gold? Still climbing.

According to NerdWallet, top high-yield savings accounts now pay up to 4.35% APY, down from 5%+ earlier in 2025. Meanwhile, gold hit $4,550/oz—an all-time high—representing a 70% gain year-to-date according to Yahoo Finance.

This isn’t about abandoning savings accounts. It’s about understanding what each asset actually does for your wealth—and making smarter allocations in a falling-rate environment.

The 2025 Reality Check: Gold vs Savings Accounts

| Metric | High-Yield Savings | Gold | Winner |

|---|---|---|---|

| 2025 Return | 4-5% APY | +70% | Gold |

| Inflation (2.7%) Beat | Barely (+1.3%) | Massively (+67%) | Gold |

| Liquidity | Instant | Same-day to 3 days | Tie |

| FDIC Insurance | Yes, $250K | No (but tangible) | Depends |

| Fed Rate Sensitivity | Falls with rates | Rises with cuts | Gold |

| Tax Treatment | Ordinary income | 28% max (collectibles) | HYSA |

Sources: Bankrate, Yahoo Finance

Current Market Snapshot

| Asset | Current | 2025 YTD | Real Return (After 2.7% Inflation) |

|---|---|---|---|

| Gold Spot | $4,550/oz | +70% | +67.3% |

| Best HYSA | 4.35% APY | +4.35% | +1.65% |

| Average HYSA | 4.00% APY | +4.00% | +1.30% |

| National Average Savings | 0.39% APY | +0.39% | -2.31% |

| 24K Gold (India) | ₹1,40,030/10g | +75% | +72.3% |

Sources: Bankrate, GoodReturns, BLS CPI Data

Why High-Yield Savings Rates Are Falling

According to NerdWallet, savings account rates have been steadily declining throughout 2025:

Rate Decline Timeline

| Date | Top HYSA Rate | Fed Funds Rate | Source |

|---|---|---|---|

| Jan 2025 | 5.00%+ | 4.50-4.75% | Bankrate |

| Jun 2025 | 4.75% | 4.25-4.50% | Bankrate |

| Oct 2025 | 4.50% | 3.75-4.00% | Federal Reserve |

| Dec 2025 | 4.35% | 3.50-3.75% | NerdWallet |

“As the Fed continues cutting rates, savers will begin to see the yield they earn dwindle. Interest rates are expected to fall one percent by mid-2026.” — Yahoo Finance

The Fed’s Impact

The Federal Reserve cut rates by 25 basis points on December 10, 2025, bringing the federal funds rate to 3.50%-3.75%. This was the third rate cut of 2025:

| Fed Meeting | Action | New Rate |

|---|---|---|

| Sep 2025 | -50 bps | 4.25-4.50% |

| Oct 2025 | -25 bps | 3.75-4.00% |

| Dec 2025 | -25 bps | 3.50-3.75% |

According to the Fed’s dot plot, only one additional cut is expected in 2026, but markets anticipate savings rates will continue falling as banks adjust to the lower rate environment.

Why Gold Thrives When Savings Rates Fall

Gold and interest rates have a well-documented inverse relationship. According to VanEck, gold performs best in falling-rate environments for three key reasons:

1. Opportunity Cost Disappears

When savings accounts pay 5%, holding gold means forfeiting that yield. When rates drop to 3-4%, the cost of holding gold shrinks dramatically.

| Rate Environment | HYSA Yield | Gold Opportunity Cost | Gold Appeal |

|---|---|---|---|

| High rates (5%+) | 5.00% | High | Lower |

| Moderate rates (4%) | 4.00% | Moderate | Neutral |

| Low rates (2-3%) | 2.50% | Low | Higher |

| Zero rates | 0.10% | Negligible | Maximum |

2. Dollar Weakness

Fed rate cuts typically weaken the US dollar, making gold cheaper for international buyers. According to BlackRock, this dynamic has been a significant driver of gold’s 2025 rally.

3. Real Rates Turn Negative

When inflation (2.7%) exceeds savings yields (4%), real returns are positive but shrinking. When real rates are negative, gold becomes essential for wealth preservation.

| Scenario | Nominal Rate | Inflation | Real Rate | Gold Outlook |

|---|---|---|---|---|

| 2023 Peak | 5.50% | 3.40% | +2.10% | Neutral |

| Dec 2025 | 4.00% | 2.70% | +1.30% | Positive |

| 2026 Forecast | 3.00% | 2.50% | +0.50% | Very Positive |

The Inflation Hedge Reality

According to Kinesis Money, gold has proven to be a superior inflation hedge over the long term:

Long-Term Performance Comparison

| Period | Gold Return | HYSA Equivalent | Inflation | Gold Real Return |

|---|---|---|---|---|

| 2025 YTD | +70% | +4% | 2.7% | +67% |

| 5 Years (2020-2025) | +125% | +15% (avg) | +18% | +107% |

| 10 Years (2015-2025) | +180% | +20% (avg) | +28% | +152% |

| 20 Years (2005-2025) | +550% | +35% (avg) | +55% | +495% |

Source: Gainesville Coins

“Gold can offer protection against inflation, as its value tends to rise as currencies become weaker. Since the supply of gold is inherently limited, its value tends to hold steady during periods of economic turbulence.” — The Smart Investor

The 2025 Inflation Battle

According to BLS data, November 2025 CPI showed:

- Overall inflation: 2.7%

- Core inflation: 2.6%

- Shelter: +3.0%

- Electricity: +6.9%

- Coffee: +19%

- Beef: +21%

With a 4% HYSA, your real return after inflation is just 1.3%. With gold’s 70% return, your real return is 67.3%. That’s a 50x difference in inflation-adjusted wealth building.

The Liquidity Myth

Many people choose savings accounts because they believe gold isn’t liquid. This is outdated thinking.

Liquidity Comparison

| Factor | High-Yield Savings | Digital Gold | Physical Gold |

|---|---|---|---|

| Access time | Instant | Minutes to hours | 1-3 days |

| 24/7 availability | Yes (online) | Yes | No (dealers) |

| Minimum sale | $0.01 | $1 | Varies |

| Transaction cost | $0 | 0.5-1% | 3-5% |

| Global access | US banks only | Worldwide | Worldwide |

According to MMTC-PAMP, digital gold can be sold 24/7 with proceeds deposited within hours.

“You can sell your digital gold 24/7, directly from your phone. In a medical emergency or sudden cash crunch, that kind of speed can make a huge difference.” — InCred Money

When Savings Accounts Still Make Sense

High-yield savings accounts aren’t useless. According to financial experts at CNBC, they serve specific purposes:

Best Use Cases for HYSA

| Use Case | Why HYSA Works | Gold Alternative |

|---|---|---|

| Emergency fund (first 3 months) | Instant access, FDIC insured | Not recommended |

| Short-term goals (under 1 year) | No volatility risk | Only if comfortable with price swings |

| Down payment savings | Predictable value | Can add gold hedge portion |

| Operating cash | Daily liquidity needs | Not practical |

HYSA Limitations

| Limitation | Impact | Gold Solution |

|---|---|---|

| Rate follows Fed cuts | Falling income | Gold rises when rates fall |

| Inflation erosion | 1.3% real return | 67% real return in 2025 |

| No upside | Maximum gain is APY | Unlimited appreciation potential |

| Currency risk | Dollar only | Global value |

The Optimal Allocation: HYSA + Gold

According to Digit Insurance, financial experts recommend a balanced approach:

Recommended Allocation Framework

| Component | Percentage | Purpose | Expected Return |

|---|---|---|---|

| HYSA | 40-50% | Immediate liquidity | 4% nominal |

| Liquid mutual funds | 20-30% | Higher returns | 6-8% |

| Digital gold | 10-20% | Inflation hedge + growth | Variable |

| Physical gold | 5-10% | Long-term store of value | Variable |

By Goal Timeline

| Timeline | HYSA Weight | Gold Weight | Rationale |

|---|---|---|---|

| under 1 year | 80-90% | 10-20% | Stability priority |

| 1-3 years | 60-70% | 30-40% | Balanced approach |

| 3-5 years | 40-50% | 50-60% | Growth priority |

| 5+ years | 20-30% | 70-80% | Maximum appreciation |

2026 Outlook: Why Gold May Extend Its Lead

According to J.P. Morgan Research, the gold vs savings gap could widen in 2026:

Projected Returns

| Asset | 2026 Projection | Basis |

|---|---|---|

| Gold | +10-20% (to $5,000/oz) | Central bank buying, ETF inflows |

| HYSA | 3.0-3.5% | Fed expected to cut once more |

| Inflation | 2.5-3.0% | Fed’s target trajectory |

| Gold Real Return | +7-17% | Assuming 2.5% inflation |

| HYSA Real Return | +0.5-1.0% | Assuming 2.5% inflation |

“Central bank and investor demand for gold is set to remain strong, averaging 585 tonnes per quarter in 2026. Prices are expected to push toward $5,000/oz by Q4 2026.” — J.P. Morgan

Key Drivers for 2026

| Factor | Impact on Gold | Impact on HYSA |

|---|---|---|

| Fed rate cuts | Positive | Negative |

| Central bank buying | Positive | Neutral |

| Geopolitical tensions | Positive | Neutral |

| Dollar weakness | Positive | Negative |

| Inflation persistence | Positive | Erosion |

Tax Considerations

Before shifting from savings to gold, understand the tax implications:

Tax Comparison

| Factor | HYSA | Physical Gold | Gold ETF (GLD) | Gold IRA |

|---|---|---|---|---|

| Tax rate | Ordinary income | 28% max (collectibles) | 28% max | Tax-deferred/free |

| Annual reporting | 1099-INT | None until sold | 1099-B | None until withdrawal |

| State tax | Yes | Varies by state | Yes | Depends on IRA type |

| Holding period benefit | None | None | None | Long-term deferral |

Source: Bankrate

For NRIs, consult a tax professional about FBAR reporting requirements for foreign gold holdings.

The Bottom Line

The numbers tell the story:

| 2025 Performance | HYSA | Gold |

|---|---|---|

| Nominal return | +4% | +70% |

| After inflation (2.7%) | +1.3% | +67.3% |

| $10,000 became | $10,400 | $17,000 |

High-yield savings accounts serve a purpose—emergency funds, short-term goals, and operating cash. But if you’re keeping significant wealth in a 4% APY account while gold delivers 70% returns, you’re choosing safety over prosperity.

The Fed’s rate-cutting cycle is just beginning. Every cut makes your savings account less attractive and gold more appealing. The question isn’t whether to own gold—it’s how much of your wealth should be in an asset that actually builds purchasing power.

A 4% savings rate can’t compete with 70% gold returns. And as rates fall further, that gap will only widen.

Start Building Real Wealth with Mantra Mint

Your savings account earned 4%. Gold returned 70%. The difference? $6,000 on a $10,000 investment.

Why Gold Beats Savings in 2025:

- Gold +70% vs HYSA +4%

- Real return: +67% vs +1.3%

- Rising as Fed cuts vs Falling with rates

- No yield cap — unlimited upside

Why Mantra Mint?

- Start with $10 — Build your gold position gradually

- Instant liquidity — Sell anytime, like a savings account

- 24/7 access — Check your holdings anytime

- No minimums — Unlike many gold dealers

Stop settling for 4% when gold offers 70%. Start building real purchasing power today.

Start Buying Gold Now — Beat the savings account trap.

Sources

- NerdWallet - Best High-Yield Savings Accounts

- Bankrate - Best High-Yield Savings Accounts

- Yahoo Finance - Gold Futures

- Federal Reserve - FOMC Statement December 2025

- BLS - Consumer Price Index

- VanEck - Gold in 2025

- BlackRock - Stay Long Gold

- J.P. Morgan - Gold Price Predictions

- Kinesis Money - Gold vs Savings Accounts

- Gainesville Coins - Gold as Inflation Hedge

- The Smart Investor - Savings Account vs Gold

- GoodReturns - Gold Rate Today

- CNBC - CPI Inflation November 2025

Ready to start investing in gold?

Join thousands of Indian families building wealth with Mantra Mint.

Get Started Free