Gold Gifts for Children: Why Gold May Beat a 529 Plan for Your Child's Future

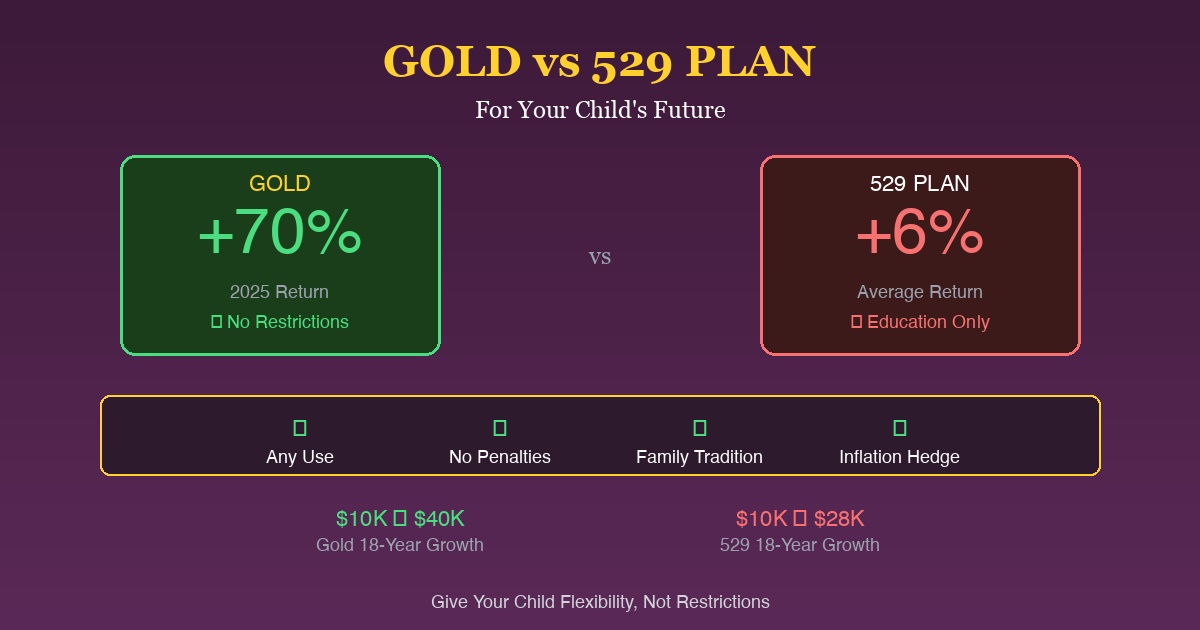

This holiday season, grandparents across America are writing checks to 529 college savings plans. But here’s what they’re missing: while 529 plans average 6% annual returns, gold delivered 70% in 2025 alone. More importantly, gold comes with zero restrictions on how your child can use it—unlike the rigid rules governing 529 withdrawals.

According to Morningstar, even the top-rated 529 plans can’t match gold’s 2025 performance. And according to NerdWallet, children can own gold through UTMA custodial accounts with full flexibility to use the assets for any purpose—not just education.

For Indian families who’ve passed gold through generations, this isn’t news. It’s tradition meeting modern wealth building.

The 2025 Performance Gap

| Investment | 2025 Return | 10-Year CAGR | Flexibility | Tax Treatment |

|---|---|---|---|---|

| Gold | +70% | +12% | Full | 28% max on gains |

| Best 529 Plans | +8-12% | +6% avg | Education only | Tax-free if qualified |

| Average 529 | +6% | +5% avg | Education only | Penalties if non-qualified |

| S&P 500 Index | +18% | +11% | Full | Capital gains rates |

Sources: Yahoo Finance, Morningstar, Saving for College

How 529 Plans Work (And Their Limitations)

According to the IRS, 529 plans offer tax-advantaged savings for education expenses. But the restrictions are significant:

529 Plan Rules

| Feature | Benefit | Limitation |

|---|---|---|

| Tax-free growth | Earnings compound tax-free | Only if used for education |

| Tax-free withdrawals | No tax on qualified expenses | 10% penalty + tax on non-qualified |

| State tax deduction | Up to 5% average | Only in your state’s plan |

| Contribution limits | High ($300K-$500K total) | Subject to gift tax rules |

Source: Fidelity

What Happens If Your Child Doesn’t Go to College?

According to Edward Jones:

| Scenario | 529 Outcome | Gold Outcome |

|---|---|---|

| Child skips college | 10% penalty + income tax on earnings | No penalty, full access |

| Child gets scholarships | Can withdraw scholarship amount penalty-free | Already has gold, use for anything |

| Child starts a business | Penalty unless it’s a qualified apprenticeship | Perfect startup capital |

| Child buys a home | 10% penalty | Perfect down payment |

| Different career path | Must change beneficiary or pay penalties | No restrictions |

The New 529-to-Roth IRA Rollover

According to the SECURE 2.0 Act, starting in 2024, unused 529 funds can roll over to a Roth IRA:

| Rule | Limitation |

|---|---|

| Account age | Must be open 15+ years |

| Lifetime cap | $35,000 maximum rollover |

| Annual limit | Subject to IRA contribution limits |

| Beneficiary | Must be the 529 beneficiary |

This helps, but gold offers immediate flexibility without a 15-year waiting period.

Why Gold for Children Makes Sense

1. No Usage Restrictions

According to Vanguard, UTMA custodial accounts allow children to use assets for any purpose once they reach the age of majority:

| Feature | 529 Plan | UTMA with Gold |

|---|---|---|

| College expenses | ✓ Tax-free | ✓ Fully accessible |

| Vocational training | Limited | ✓ Fully accessible |

| Starting a business | ✗ Penalized | ✓ Perfect for this |

| Buying a car | ✗ Penalized | ✓ Fully accessible |

| First home down payment | ✗ Penalized | ✓ Fully accessible |

| Emergency fund | ✗ Penalized | ✓ Fully accessible |

| Investment capital | ✗ Penalized | ✓ Fully accessible |

2. Superior Long-Term Performance

Gold has outperformed most asset classes over the past two decades:

| Period | Gold Return | 529 Average | Difference |

|---|---|---|---|

| 2025 YTD | +70% | +6% | +64% |

| 5 Years (2020-2025) | +125% | +40% | +85% |

| 10 Years (2015-2025) | +180% | +80% | +100% |

| 20 Years (2005-2025) | +550% | +150% | +400% |

Source: World Gold Council, Saving for College

3. Inflation Protection

According to Gainesville Coins, gold has consistently outpaced inflation:

| Decade | Inflation | Gold Return | Real Return |

|---|---|---|---|

| 2015-2025 | +28% | +180% | +152% |

| 2005-2015 | +25% | +130% | +105% |

| 1995-2005 | +28% | +50% | +22% |

529 plans invested in bonds and conservative portfolios often barely beat inflation—meaning your child’s purchasing power may not grow meaningfully.

4. Cultural Significance for Indian Families

For Indian families, gold carries meaning beyond investment returns:

| Traditional Milestone | Gold’s Role | 529 Alternative |

|---|---|---|

| Naming ceremony (Namkaran) | Gold coin gift tradition | Check to account |

| First birthday | Gold jewelry | Check to account |

| Graduation | Gold gift of achievement | Already in 529 |

| Wedding | Gold from grandparents | Must withdraw with penalty |

| Starting life | Family gold legacy | Must use for education |

According to the World Gold Council, Indian families have gifted gold for generations—it’s wealth that tells a story.

How to Set Up Gold for Your Child

Option 1: UTMA Custodial Account with Gold

According to Fidelity, UTMA accounts can hold tangible assets including gold:

| Feature | Details |

|---|---|

| Who opens | Parent or guardian as custodian |

| Who owns | Child (you manage until majority) |

| Age of transfer | 18-25 depending on state |

| Tax treatment | First $1,350 tax-free, next $1,350 at child’s rate |

| Investment options | Stocks, bonds, gold, any asset |

Steps to open:

- Open UTMA account at brokerage that allows gold

- Purchase gold ETF (GLD, IAU) or gold funds

- Or use digital gold platform like Mantra Mint

- Manage until child reaches majority

Option 2: Digital Gold Account

For maximum flexibility and lowest minimums:

| Feature | Digital Gold | Physical Gold |

|---|---|---|

| Minimum investment | $10 | $200+ |

| Storage costs | None or minimal | Safe deposit or home |

| Liquidity | Instant | Must find buyer |

| Divisibility | Any amount | Fixed denominations |

| Insurance | Included | Your responsibility |

Option 3: Physical Gold Gifts

Traditional physical gold remains powerful:

| Gift Type | Typical Amount | Occasion |

|---|---|---|

| Gold coin (1g-5g) | $100-$500 | Birthdays, milestones |

| Gold chain | $500-$2,000 | Significant birthdays |

| Gold jewelry set | $2,000+ | Major milestones |

Tax Considerations: Gold vs 529

Gift Tax Rules for 2025

According to the IRS, both gold gifts and 529 contributions follow the same gift tax rules:

| Rule | 2025 Limit | Application |

|---|---|---|

| Annual exclusion | $19,000/person | Per child, per year |

| Married couple | $38,000/child | Combined gift |

| 529 superfunding | $95,000 | 5-year election |

| Lifetime exclusion | $13.61 million | Above annual limits |

Source: Fidelity

Tax on Growth

| Investment | Tax on Growth | Tax on Withdrawal |

|---|---|---|

| 529 (qualified use) | None | None |

| 529 (non-qualified) | Ordinary income | 10% penalty |

| Gold in UTMA | Child’s rate up to $2,700 | 28% max collectibles rate |

| Gold in taxable | Capital gains | 28% max collectibles rate |

The “Kiddie Tax” for UTMA Accounts

According to NerdWallet:

| 2025 UTMA Earnings | Tax Rate |

|---|---|

| First $1,350 | Tax-free |

| $1,350 - $2,700 | Child’s rate (10%) |

| Above $2,700 | Parent’s marginal rate |

For long-term gold holdings, most gains are deferred until sale—often after the child is an adult with their own (potentially lower) tax bracket.

The Math: $10,000 Gift Comparison

Let’s compare a $10,000 gift today, held for 18 years:

Scenario 1: 529 Plan (6% Average Return)

| Year | Balance | Notes |

|---|---|---|

| 0 | $10,000 | Initial gift |

| 5 | $13,382 | 6% CAGR |

| 10 | $17,908 | 6% CAGR |

| 18 | $28,543 | Tax-free if for education |

Outcome: $28,543 for college only, or $25,689 after penalties for other uses.

Scenario 2: Gold (Historical 8% CAGR)

| Year | Balance | Notes |

|---|---|---|

| 0 | $10,000 | Initial gift |

| 5 | $14,693 | 8% CAGR |

| 10 | $21,589 | 8% CAGR |

| 18 | $39,960 | Any use, no restrictions |

Outcome: $39,960 for anything—college, business, home, or continued growth.

Scenario 3: Gold (2025 Performance Continues at 10% CAGR)

| Year | Balance | Notes |

|---|---|---|

| 0 | $10,000 | Initial gift |

| 5 | $16,105 | 10% CAGR |

| 10 | $25,937 | 10% CAGR |

| 18 | $55,599 | Any use, no restrictions |

Outcome: $55,599 with full flexibility.

When 529 Plans Still Make Sense

To be fair, 529 plans have genuine advantages:

| Advantage | Who Benefits |

|---|---|

| State tax deduction | High-income families in high-tax states |

| Guaranteed college path | Children certain to attend college |

| Medicaid protection | Some states exempt 529s from Medicaid |

| Grandparent contributions | Reduced financial aid impact (new rules) |

Consider 529 if:

- You’re confident your child will attend college

- You’re in a high state tax bracket

- You’ve maxed out other tax-advantaged accounts

- Your child is unlikely to receive scholarships

Consider gold if:

- You want maximum flexibility

- You value inflation protection

- You want to continue Indian family traditions

- Your child’s path is uncertain

- You want to build generational wealth

The Hybrid Strategy: Best of Both

For families who want security and flexibility:

| Allocation | Purpose | Vehicle |

|---|---|---|

| 50% | Core education fund | 529 Plan |

| 30% | Flexible wealth building | Gold (UTMA) |

| 20% | Emergency/opportunity | Digital gold |

This ensures:

- Tax-free growth for education expenses

- Flexible capital for any opportunity

- Inflation hedge and generational wealth

Holiday Gold Gifting: Making It Meaningful

This holiday season, consider gold over toys:

Gift Ideas by Budget

| Budget | Physical Gift | Digital Option |

|---|---|---|

| $50-100 | 1g gold coin | Digital gold balance |

| $100-500 | 5g gold bar | Digital gold + certificate |

| $500-1,000 | 10g gold bar or jewelry | Digital gold fund |

| $1,000+ | Gold jewelry or bars | UTMA gold portfolio |

Creating a Gold Gifting Tradition

| Occasion | Suggested Gift | Meaning |

|---|---|---|

| Birth | First gold coin | Welcome to the family |

| Birthdays | Add to collection | Annual wealth building |

| Graduations | Significant gold gift | Achievement recognition |

| Life milestones | Family heirloom | Continuation of tradition |

The Bottom Line

529 plans are fine for families certain about traditional college paths. But gold offers something more:

| Factor | 529 Plan | Gold |

|---|---|---|

| 2025 Performance | +6% | +70% |

| Flexibility | Education only | Any use |

| Restrictions | Penalties for non-education | None |

| Cultural significance | Check to account | Generational tradition |

| Inflation protection | Limited | Proven over 50+ years |

| Child’s autonomy | Limited to education | Full freedom |

For Indian families especially, gold isn’t just an investment—it’s a connection to heritage, a symbol of love, and a foundation for whatever path your child chooses.

Your grandmother didn’t save 529 plan contributions. She saved gold. And her gift is still valuable today.

Give the Gift of Gold This Holiday Season with Mantra Mint

529 plans restrict. Gold empowers. Give your child or grandchild the gift of flexibility.

Why Gold Over 529 Plans:

- +70% in 2025 vs 6% for 529s

- No restrictions — use for anything, not just college

- Generational wealth — continues Indian family traditions

- Inflation protection — proven over 50+ years

Why Mantra Mint?

- Start with $10 — Perfect for recurring gifts

- No minimums — Gift any amount

- UTMA-friendly — Set up custodial accounts

- Instant access — Buy and gift in minutes

This holiday season, give a gift that grows and lasts. Start building your child’s gold legacy today.

Start Gifting Gold — Better than a 529, more meaningful than a toy.

Sources

- Morningstar - 529 Ratings Best Plans

- NerdWallet - Best Custodial Accounts

- Vanguard - UGMA-UTMA Accounts

- Fidelity - Custodial Accounts

- IRS - 529 Plans Questions and Answers

- Edward Jones - Unused 529 Funds

- Saving for College - 529 Performance Rankings

- World Gold Council - Gold Prices

- Yahoo Finance - Gold Futures

- Gainesville Coins - Gold Inflation Hedge

- CNBC - Best Investment Accounts for Kids

Ready to start investing in gold?

Join thousands of Indian families building wealth with Mantra Mint.

Get Started Free